Low returns, inflation pose immediate threat to state finances

The Alaska Permanent Fund, now valued at near $80 billion, is not about to run out of money.

But the so-called earnings reserve of the fund, which is the only portion that the Legislature can appropriate for paying dividends and running state government, could run out of money in a few years if inflation remains a problem and investment returns are low.

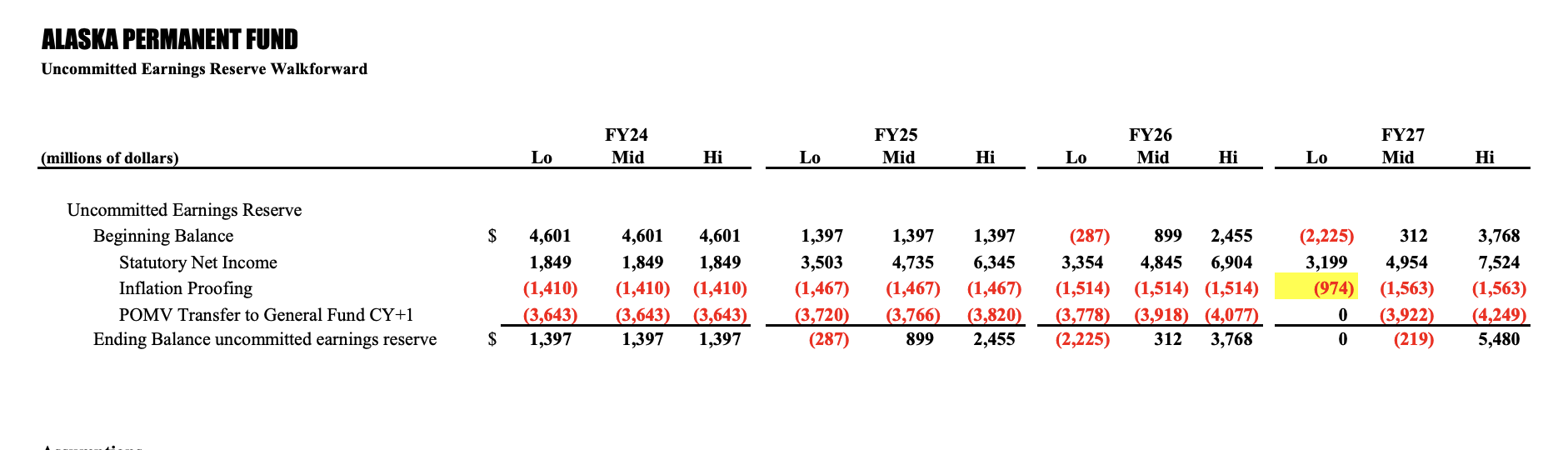

The chart below, presented to the Permanent Fund trustees July 12, shows how things might play out under three alternative visions of the immediate future.

In each case, inflation is assumed to be 2.5 percent, which is low. If inflation is higher than that, the real returns will be worse.

High returns would temporarily hide the unsustainable nature of the situation. But moderate returns, low returns or outright losses—which are possible—will push the earnings reserve into the red.

By July 2026, low returns would mean underfunding inflation proofing by $600 million and no funds that could be transferred to pay for a dividend or much of state government in fiscal year 2027.

Note the numbers for fiscal year 2025, which begins in 11 months, showing a negative $287 million in the reserve by the summer of 2026. That would be after transferring $3.7 billion to pay for dividends and run state government from July 2024 to June 2025.

The chart above and the presentation at the meeting that led to the news stories saying the earnings reserve could be out of spendable money in three or four years.

The state adopted a law in 2018 under which the annual transfer from the earnings reserve is equal to a 5 percent average of the total fund value over the past five years. The withdrawal has to be taken from the earnings reserve, which is a small part of the overall fund.

But when the earnings reserve shrinks to the point where it can’t pay the bills, the problem can no longer be disguised.

The first target will be the inflation-proofing deposit. The chart shows an annual transfer of about $1.4 billion from the earnings reserve into the principal.

Some will claim that inflation proofing is not justified because the state deposited money into the principal of the fund in the past, including the $4 billion transfer that the Legislature approved in 2021.

Gov. Mike Dunleavy claimed that he vetoed the transfer, but his administration made a mistake in the official document he signed, so the transfer took place, despite his opposition.

The Legislature has made periodic deposits to the principal for more than 40 years, starting with $900 million in 1980. The idea that a past deposit erases the need for future inflation proofing is arbitrary and runs counter to past practice.

It would weaken the support for inflation proofing, which is the only mechanism for ensuring that future generations will share in the wealth generated by the nonrenewable North Slope oil bonanza.

Eliminating or reducing inflation proofing will be pushed by those who claim we don’t need new taxes and that everything with the fund is fine.

The annual Percent of Market Value transfer to the general fund, in the $3.6 billion range in the chart, reflects the total amount available for dividends and running the government. The dividend this year is $1,300, which is about $900 million of that total, meaning $2.7 billion to pay for government services. That is about half of the state budget.

The potential for low returns and inflation poses an immediate threat to state finances, but Dunleavy, who campaigned in 2022 on the theme that we had no money problems, has yet to come to grips with the challenge.

The pending shortfall in the earnings reserve is one of many reasons why the state needs a fiscal plan, which has to start with leadership by the governor. The pending shortfall also points to the antiquated structure of the Permanent Fund and the need for a constitutional amendment to modernize the system so that it contains a single account from which a fixed percentage of assets can be spent each year.

More than 30 years ago, former Rep. Hugh Malone argued for a better system with a set percentage payout, but the hysteria that accompanies any measure dealing with the Permanent Fund stalled progress and allowed inertia to rule the day.

Shortly before discussing the earnings reserve forecast at its July 12th meeting, there was a complaint by one trustee about the requirement for public meetings in Alaska. The solution is not, as Jason Brune claims, to allow more secrecy, but to do a better job in making Permanent Fund operations more transparent. It’s no great hardship to have more meetings and give public notice.

Your contributions help support independent analysis and political commentary by Alaska reporter and author Dermot Cole. Thank you for reading and for your support. Either click here to use PayPal or send checks to: Dermot Cole, Box 10673, Fairbanks, AK 99710-0673.

The discussion about the earnings reserve starts 31 minutes and 50 seconds into the meeting.